Cell & Gene Therapy Manufacturing Bottlenecks 2025: Investment Strategies in CDMOs, Viral Vector Capacity, and Regulatory Fast-Track Winners

- Dr. TiehKoun Koh

- May 28

- 3 min read

Cell and gene therapy (CGT) has entered a new era. The FDA approved seven new cell and gene therapies in 2024–2025, including Abeona’s ZEVASKYN and Novartis’s ITVISMA. These curative treatments are no longer science fiction – they are reaching patients.

But here is the problem that smart investors are watching closely: manufacturing is failing.

According to industry data, up to 74% of biotech startup failures trace back to poor Chemistry, Manufacturing, and Controls (CMC) strategy. Scaling a lentiviral vector or CAR-T process from lab-scale to commercial GMP production remains a graveyard for well-funded science.

For institutional investors, family offices, and pharma strategists, this bottleneck is not a risk – it is the single largest investment opportunity in life sciences today.

---

Why the Bottleneck Is Worse Than You Think

Unlike small molecule drugs, CGT products are living medicines. Each patient batch is essentially a unique manufacturing run. The three critical pain points driving returns:

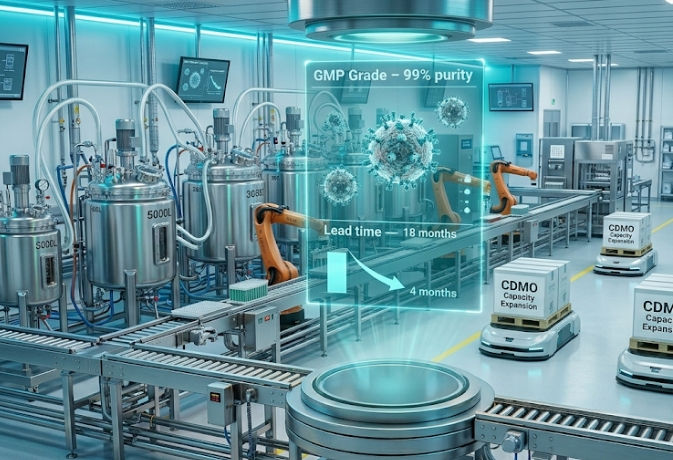

1. Viral Vector Capacity Crunch

Nearly 70% of cell and gene therapies rely on viral vectors (AAV, lentivirus). Global GMP-grade vector supply is constrained, with lead times stretching 12–18 months. Companies without secured vector capacity face silent clinical holds.

2. Manual, Error-Prone Processing

Most CGT manufacturing still uses open, manual systems. Contamination risk is high, and labor costs explode. The shift toward automated closed-loop systems (e.g., automated cell processing platforms) is no longer optional – it is a competitive necessity.

3. Severe GMP Workforce Shortage

The US alone needs 25,000+ new bioprocessing technicians by 2030. Over half of all CGT manufacturers report critical gaps in GMP-trained staff. A new facility can open but remain idle without qualified operators.

---

The Investment Angle: Where Capital Is FlowThe Investment Angle: Where Capital Is Flowing

Big pharma and venture capital are paying premium multiples for de-risked manufacturing solutions.

Investment Target Rationale Recent Signals

CDMOs (Contract Development & Manufacturing Organizations) Outsourcing is accelerating. The CGT CDMO market is projected to grow at 23% CAGR to $27.1B by 2033. Lonza, Catalent, Thermo Fisher expanding capacity.

Investor takeaway: Avoid first-generation platform companies. Look for proven commercial-scale CDMOs with multiple filed BLA/MAAs, or automation hardware already adopted by top-10 pharma.

---

Regulation Relevance: Which Countries Win?

Regulatory speed directly impacts return on capital. Countries with fast-track schemes are attracting manufacturing footprints.

United States – FDA RMAT

· Fast-track: Regenerative Medicine Advanced Therapy (RMAT) designation offers rolling reviews and intensive early guidance.

· Lead time from IND to approval: ~10–12 months (RMAT accelerated pathway)

· Verdict: Most flexible for de-risked assets.

China – NMPA 60-Day IND (30-Day for priority)

· Fast-track: Tacit approval – if no objection within 60 days (30 for priority assets), trial may proceed.

· Lead time: Fastest “paper approval” globally.

· Verdict: Ideal for CDMOs serving both domestic and global trials.

Singapore – HSA Abridged Pathway

· Fast-track: ~320-day evaluation for products already approved by FDA/EMA/PMDA.

· Lead time: Longer than US/China but serves as ASEAN gateway.

· Verdict: Pragmatic secondary hub for global CDMOs.

Switzerland – Swissmedic

· Fast-track: 60-day review for clinical trial applications; high compliance standards.

· Lead time: Efficient but not accelerated for commercial approval.

· Verdict: Strong for EU gateway strategies.

Regulatory insight: China’s 60-day IND is the most aggressive clock. But for manufacturing investment, the US RMAT pathway offers the most strategic flexibility because of its surrogate endpoint approvals.

---

Workforce Tie-In: The Hidden Investment Lever

Even the best automated platform fails without skilled staff. Investors are now scoring countries by biomanufacturing training infrastructure.

Winning model: Ireland’s NIBRT (National Institute for Bioprocessing Research and Training)

· €21M investment

· Trains 5,000+ professionals annually

· Directly linked to IDA Ireland’s foreign direct investment wins (e.g., Pfizer, Merck, BMS expansions)

What this means for you:

When evaluating a CGT manufacturing asset – CDMO, equipment provider, or pharma site – ask: What is the local pipeline of GMP technicians? Regions with apprenticeship-linked training centers (Ireland, Singapore, North Carolina’s BTEC) command lower labor risk premiums.

---

Summary: A Blueprint for Strategic Investment

Cell and gene therapy manufacturing is no longer a technical footnote – it is the primary value driver for the next five years.

For NY Kingfisher Associates clients, we recommend three actions:

1. Allocate 15–20% of life sciences dry powder to CDMO equity or debt vehicles focused on viral vector capacity.

2. Monitor regulatory arbitrage – China for speed, US for flexibility, Ireland for talent.

3. Avoid single-asset CGT developers unless they have a proven, scaled manufacturing partner.

The first therapy to market wins – but only if it can be made at scale.

Ready to discuss CGT manufacturing investments?

Contact NY Kingfisher Associates for a confidential strategy session. We provide due diligence, site selection, and portfolio construction for institutional investors in advanced therapeutics.

This article is for informational purposes only and does not constitute investment advice. Past performance is not indicative of future results.